An analysis of intentional, strategic, and effective digital transformation

Profitable, effective, and sustainable transformation goes much further than making an app or getting a website chatbot. Similarly, onboarding new technologies just to have the latest flashy gadget is neither 100% constructive nor harmless.

Innovation methodologies stipulate that digitising and/or digitalising operations doesn’t completely guarantee an amazing return on investment, or a groundbreaking way of doing business. Sometimes, new technology just helps to sustain a business model relative to other external factors like more agile competitors or changing consumer expectations.

In this article, we explore past, present, and impending examples of digital transformation. By looking at the customer experience before the digital transformation, we can see how intentional and strategic digital transformation not only helps businesses optimise operations, but can also change how people behave in daily life. On the flip side, we can also see how failing to keep up to date can leave entire industries exposed to threats from greenfield startups, or even other industries.

Online Banking

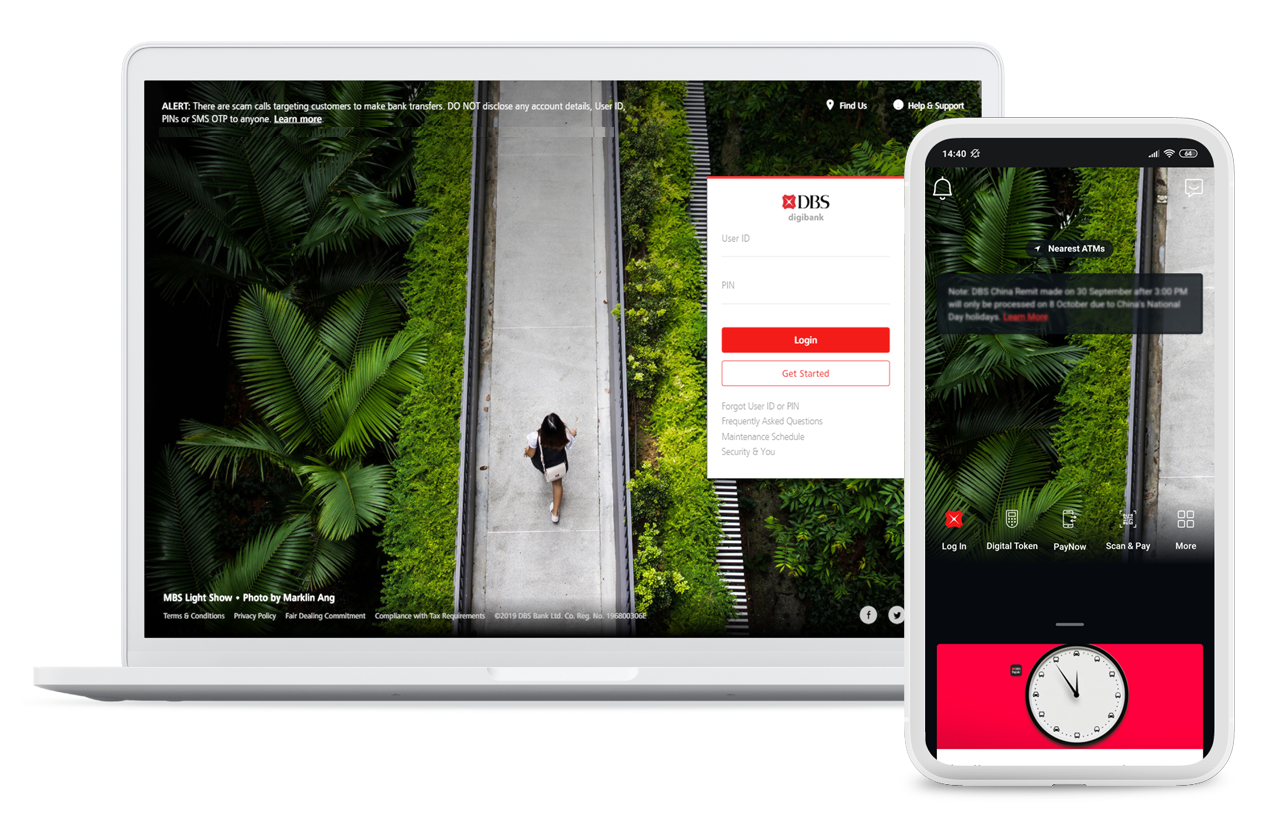

Imagine physically going to a bank every single time you need to conduct a financial transaction. Perhaps it was something you grew up doing, but in today’s perma-online world, this is becoming a foreign idea.

Banks and other financial institutions have always been quick to adopt new technologies. We can trace this pattern as far back as the shift from bartering to money, or perhaps the invention of double-entry bookkeeping by the Medicis.

More recently and broadly speaking, the consumer banking industry has continued to adapt to the “on-demand” economy very well.

For example, with online banking, most services can be done whenever and wherever a customer wants. Whether it’s something important like transferring large sums, or menial like reminding a friend about their share of that Grab you shared during a surge- the service in question is available. No more waiting for bank hours, waiting in line for the teller, or juggling physical documents.

Beyond convenience, online banking lowers the barrier to entry of financial freedom and literacy. For example, online banks (like Revolut) and traditional banks with good online services (like DBS) not only simplify banking, but also budgeting, investing, and retirement planning. With these technologies, managing finances is no longer reserved for the wealthy.

Nevertheless, the digital divide is still present. There are populations where online banking (arguably the most accessible form of banking) is still not accessible due to a lack of funds, insufficient infrastructure, cybersecurity concerns, and low financial literacy.

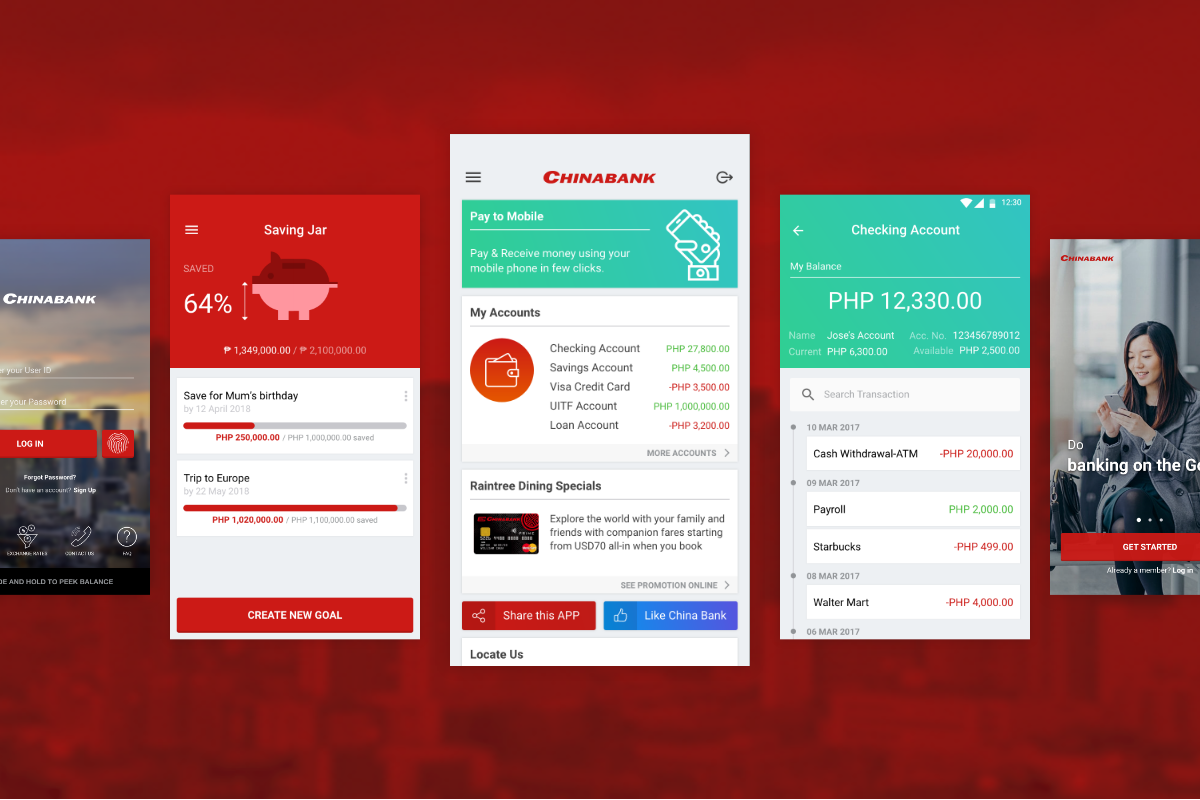

Here at Pixel Tie, we worked with Tagit and China Bank to empower the unbanked in the Philippines. In this project, digital transformation was not just about digitalising traditional banking services, but rather, making desirable and impactful online banking services for the target segment. For our client, this meant designing specific features like “Just Use your Mobile Phone” (JUMP), so that customers can transfer funds to anyone with a mobile number.

This kind of value creation required deep investigation of the target user and close collaboration with several departments in China Bank. It was about finding the intersection between our client’s goals, their customers’ needs, and the most feasible technology solutions.

Smart Supermarkets

The humble supermarket is a logistical orchestra of constantly moving parts. A supermarket has to manage: demand forecasting, inventory management, spoilage, and shrinkage, for hundreds of products.

Yet despite the breakneck speed of technological development, the customer experience of purchasing from the supermarket hasn’t changed that much over the years. Grocers seem like they’re never going to adopt new technologies. But appearances are misleading.

In fact, grocers are facing a rising cost of doing business. Consumers are also largely unwilling to compromise on quality and are coming to expect more from their grocers. These factors are coming together to leave the food retail industry with no choice but to adopt new technologies to lower margins and increase productivity.

Behind the curtain in fulfilment, internet of things (IoT), low power wide area network (LPWAN), smart boxes, dynamic pricing, and driverless vehicles help grocers manage their fleets, deliveries, and product quality.

Similarly in operations, technologies like artificial intelligence (AI), computer vision, advanced robotics, and IoT are converging to create solutions like AI-enabled predictive logistics, smart shelves, and automated temperature control.

At the point of sale, mobile apps offer features like scanners, mobile coupons, and personalisation. And in-store, some grocers are even experimenting with Bluetooth beacons to connect the physical store with mobile apps.

Nevertheless, most point-of-sale solutions are focused on automating transactional activities. A sticky behavioural byproduct of the pandemic, these solutions reduce face-to-face interaction between associates and customers. They make the customer experience feel faster and give staff more time to do other activities like stocking shelves and taking inventory.

Overall, as these digital solutions gradually reach mass adoption, grocers will be better equipped to serve shoppers without creating lots of waste. However, for the customer, these new solutions are incremental innovations. They improve the customer experience incrementally so that grocers can sustain their current business model.

There is still demand for faster and simpler customer journeys. As evidenced (in Singapore) by Grab and foodpanda, the value proposition of ordering small quantities and having it at your door in 15 minutes is a premium that consumers are willing to pay an aggregator for. And as it stands, grocers are unable to meet these expectations through their existing owned channels.

A quick aside on proprietary online channels

Online shopping is also worth noting, barring the fact that it isn’t exactly new. Digitising the catalogue and allowing customers to order their groceries from a proprietary app (or website) is a substantial channel that opens a lot of doors for both grocers and customers.

For example, customers without cars can order large amounts of groceries without worrying about the logistics of bringing them home on public transport. Using online channels, it’s also much easier to conduct routine repeat buys for household goods like toilet paper and cleaning supplies.

For grocers, proprietary online channels give them much more flexibility than a partnership with an aggregator. Furthermore, having an owned online channel allows grocers to explore digital solutions with AI-enabled hyper-personalisation, geofencing, and big data.

However, most online orders are simply not yet profitable enough for grocers to double down on proprietary online channels. With narrowing margins and the added cost of delivery, it’s proved challenging to make a profit with online channels. So, we would not expect to see any online-only grocers any time in the near future.

Insurance

For an industry that’s meant to improve our quality of life, buying insurance can be, ironically, quite painful. Like banking in the past, most activities called for interaction with a human agent. Unlike banking, however, insurance has not adapted as well to the on-demand economy.

In insurance, laggards that haven’t adopted automated self-service for consumer-facing transactional activities usually suffer for a variety of reasons.

Firstly, direct competitors that have invested in automated transactional activities provide an exponentially faster, more user-friendly, and more convenient customer experience. Secondly, companies in other industries (like Amazon, Spotify, and Netflix) are raising overall consumer expectations, especially when it comes to personalisation and speed. Thirdly, leaders in other industries (like DBS, BBVA, and Grab) are starting to enter the insurance industry with more consumer data and brand affinity than traditional insurance providers.

On another note, selling the right insurance policy the old way can have plenty of potholes for insurance providers. This is because relying on a customer to self-report their actual needs can be unreliable, leading to underselling or overselling.

And beyond the process of buying and selling insurance policies, actually executing one is similarly entrenched in an outdated way of doing business. AnswerThePublic indicates that the search query “how insurance claim works” is one of the top searches for the keyword “insurance claim” (in Singapore). So for the uninitiated consumer, filing an insurance claim can be a confusing and frustrating process.

Considering these pain points and operational deficiencies (which are, ultimately, opportunities), there are a variety of technology trends that are poised to smooth out the customer journey. These trends include artificial intelligence, distributed infrastructure, advanced connectivity, and automation- all of which are supported by trust architecture.

For example, in property and casualty insurance, insurance providers can use a combination of new technologies to automate underwriting using a wider, more precise, and more accurate range of data. This allows providers to conduct underwriting activities more efficiently, thereby improving their bottom line and reducing friction for the customer.

In life and annuities, IoT and wearable devices allow providers to engage with customers continuously (read: gather a lot more data). When combined with the aforementioned trends, policies can be turned into dynamic “umbrella” policies that adjust in step with the policyholder and span several types of coverage (life, health, critical illness, etc.).

Nevertheless, how these trends are going to play out is unclear. Will incumbents have enough room to invest in these new solutions, given the pressure from the cost of living crisis, as well as the wave of new digital-first competitors?

***

As you can see, digital transformation isn’t just a simple matter of taking on new technologies. Creating true impact means fully understanding the customer journey, the future of the industry, and the capabilities of the business.

It’s a sustained and concerted effort to transform the entirety of a business’ ecosystem, in order to deliver a fundamentally improved customer experience, with the added plus of all the new bells and whistles.

Unsure where to start?

Here at Pixel Tie, we have valuable experience designing customer journeys that make a difference. We can help you understand your customers’ pain points and turn them into business opportunities using digital solutions designed specifically for you.

If you’d like to find out how we can help future proof your business, send us an email and we’ll get to you shortly.

1 Comment

Pingback: Pixels of the Month: Ryan Reynolds, ChatGPT and Viva Magenta! - Pixel Tie